Wealth Transfer Tax — Did you know that USA IRS rules require Americans to Pay Tax at a minimum, every Quarter (4 times per year)? Taxes are due when you earn income (not end of year). Not doing so would result in tax penalties. Self Employed people or ones who own businesses already know this, but for everyone else that receives a pay stub every 2 weeks, this may be new.

When we receive our Wealth Transfer very soon, we will be required to submit a quarterly tax payment to IRS. Per the website, and attached screenshot, the first quarterly payment is due on January 15. The second payment is due June 15. So I believe this means if we receive a wealth transfer in the coming days, we will now be required to submit our quarterly tax payment on June 15 (since January 15 is pretty much here and gone already).

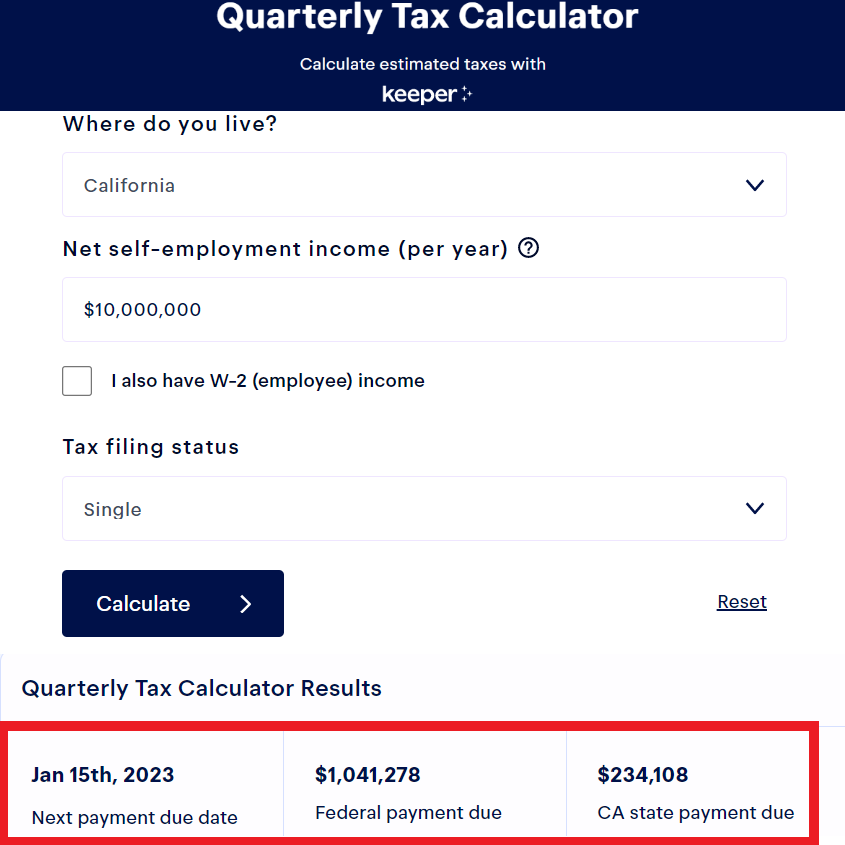

Per the Estimated Tax Calculator website/screenshot, if we make 10 million dollars in crypto and live in California, we will owe approximately $1 million dollars quarterly tax payment ($4 million total for the year) to the Federal Government and $230 thousand dollars State tax to California (so about $1 million total State tax for the year). This calculator is off a little bit because it assumes we will make our first payment on January 15 (4 quarters). But if we wait until June, we will only have 3 quarters left, so the required quarterly payment will be even higher (spread out over 3, not 4 quarters).

What happens if we don’t make this quarterly payment. The site says the underpayment penalty is equal to 0.05% of your tax due, every month that it remains unpaid. So if you have 1 million dollars quarterly tax payment, that penalty would be 500 dollars (1,000,000 * 0.05% = $500) each month that you don’t pay.

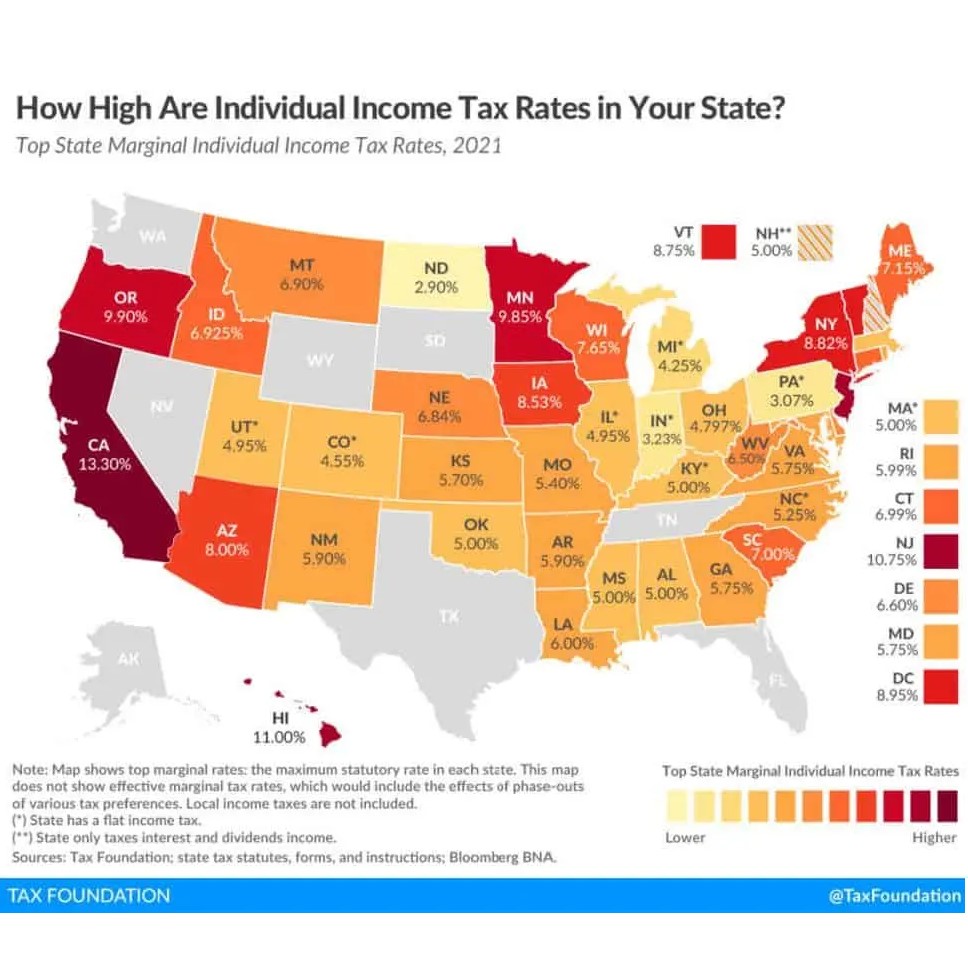

This is not financial or tax advice, but what I would do is this. As soon (same month) as the wealth transfer happens, I need to start planning to move from a State that has Income Tax, to a State without an Income Tax such as Texas, Florida, South Dakota, and a few others… I would also find a good Accountant/CPA to figure out how to reduce taxes. Because, if we wait too long, we will end up paying way higher taxes than we need to. By moving to Florida, you would not have to pay the state income tax and save millions of dollars. However, per the domicile/residency rules, you have to live in a state for 6 months or more to prove that you are a resident there (not just using it to avoid paying taxes). So this means you can’t just move to Florida in December and pretend you lived there the entire year. But again, it’s best to contact a tax professional to determine the best route to take.

https://www.keepertax.com/quarterly-tax-calculator

Penalty avoidance

This is the main reason to stay on top of your tax payments. Our tax system is based on a pay-as-you-go rule. That means taxes are due when you earn the income, not when your tax return is due.

If you don’t pay in throughout the year, you’ll likely get hit with an underpayment penalty. This penalty is equal to 0.05% of your tax due, every month that it remains unpaid.

While that might not seem like much, it can add up quickly. The best way to save your hard-earned dollars is to pay your taxes once a quarter when they’re due

https://www.irs.gov/newsroom/what-taxpayers-need-to-know-about-making-2022-estimated-tax-payments#:~:text=Aside%20from%20income%20tax%2C%20taxpayers,%2C%20and%20January%2017%2C%202023.

What taxpayers need to know about making 2022 estimated tax payments

Generally, taxpayers need to make estimated tax payments if they expect to owe $1,000 or more when they file their 2022 tax return, after adjusting for any withholding.

The remaining deadlines for paying 2022 quarterly estimated tax are: June 15, September 15, and January 17, 2023.

Anyone who pays too little tax through withholding, estimated tax payments, or a combination of the two may owe a penalty.

https://www.venturists.net/mail-forwarding-for-travelers/

As of 2021, There are currently seven states that do not have state income tax (and if you reside in those states don’t need to file a state income tax return).

https://www.irs.gov/faqs/estimated-tax

If I anticipate a sizable capital gain on the sale of an investment during the year, do I need to make a quarterly estimated tax payment during the tax year?

Generally, you must make estimated tax payments for the current tax year if both of the following apply:

You expect to owe at least $1,000 in tax for the current tax year after subtracting your withholding and refundable credits, and

You expect your withholding and refundable credits to be less than the smaller of:

90% of the tax to be shown on your current year’s tax return, or

100% of the tax shown on your prior year’s tax return. (Your prior year’s tax return must cover all 12 months.)

You may be able to annualize your income and make an estimated tax payment or an increased estimated tax payment for the quarter in which you realize the capital gain.